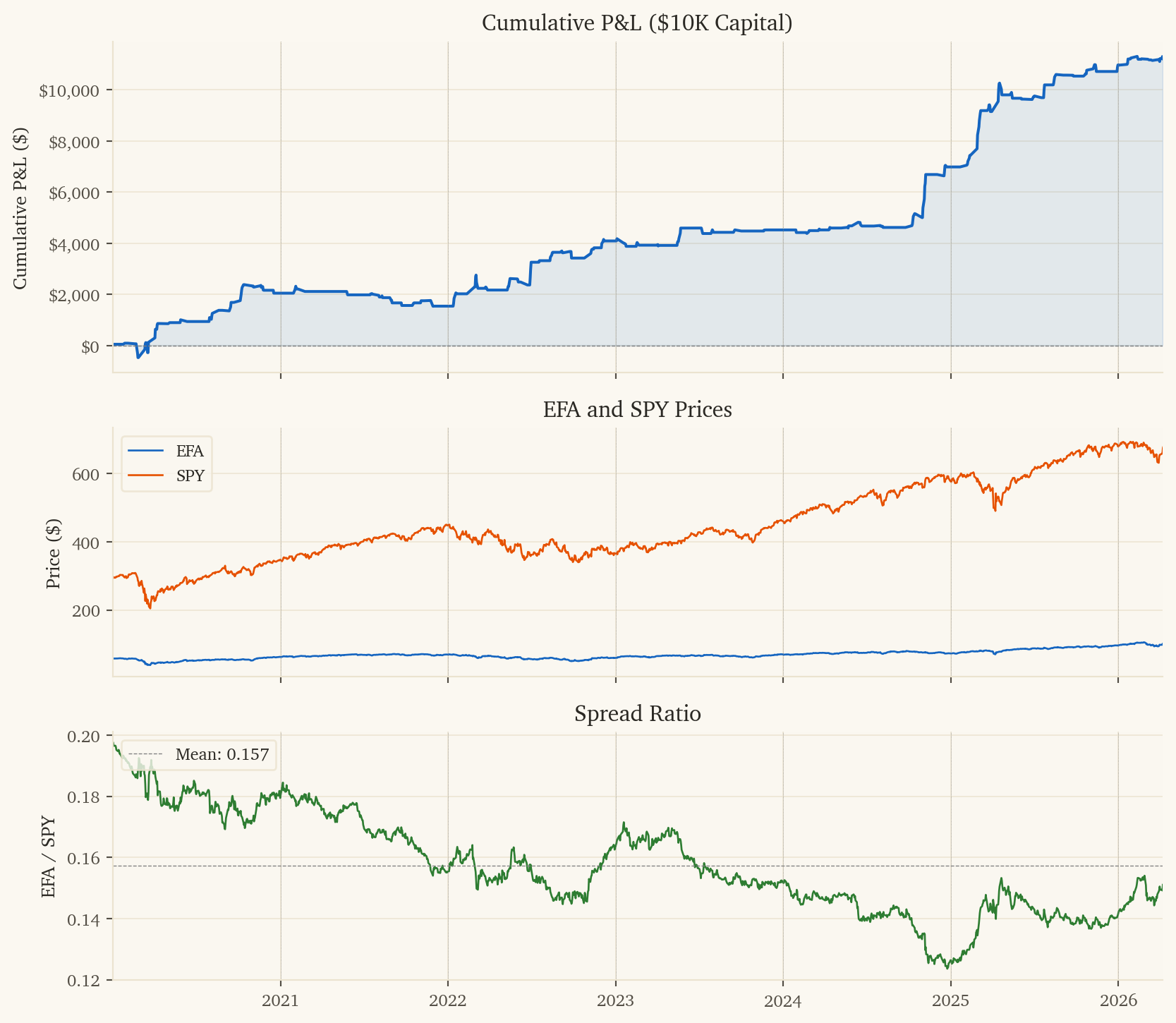

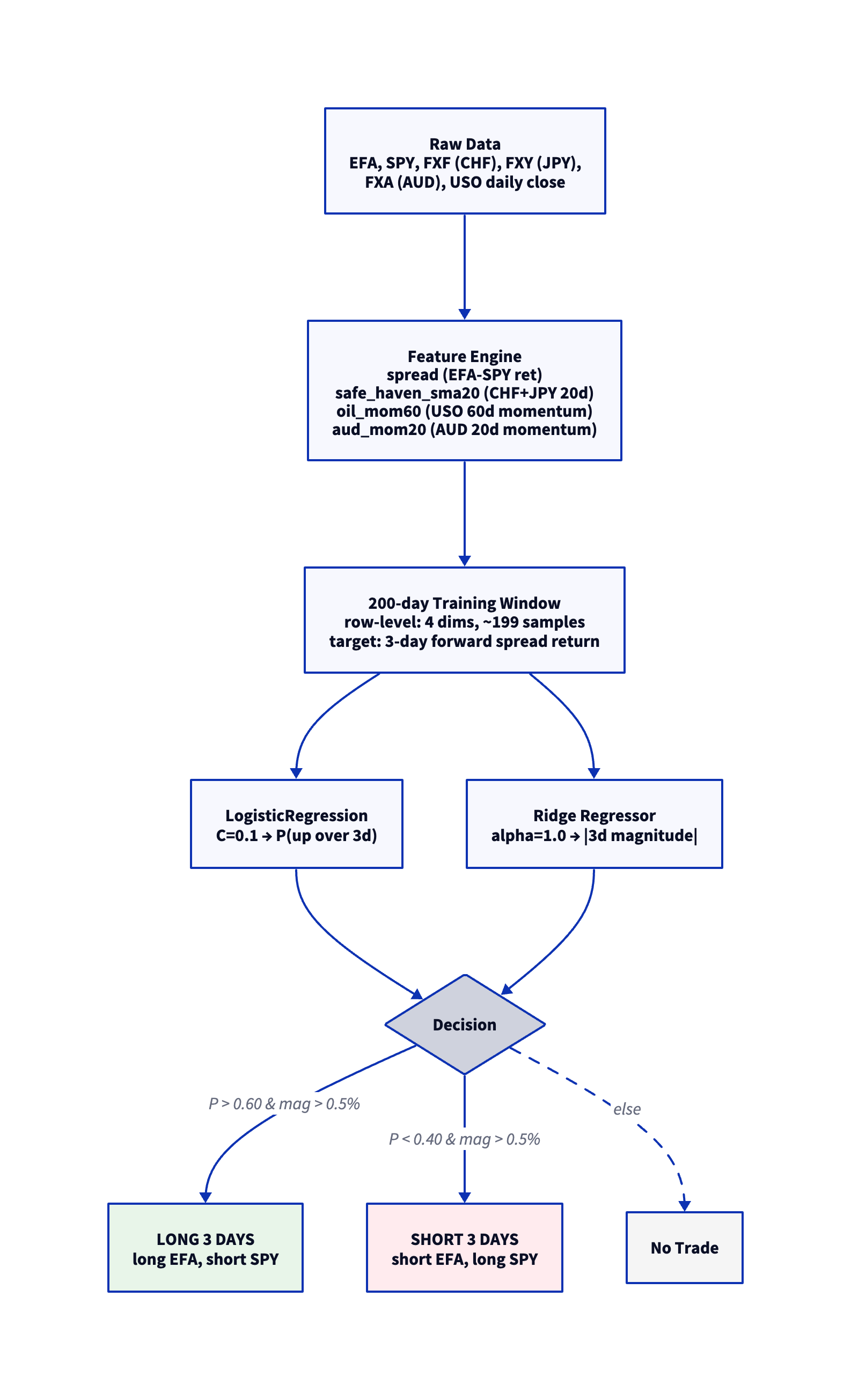

This document presents a systematic pairs trading strategy on EFA (iShares MSCI EAFE – international developed equities) vs SPY (S&P 500 – US equities). The strategy predicts 3-day forward returns of the EFA-SPY spread using safe-haven currency flows, oil momentum, and AUD momentum as signals.

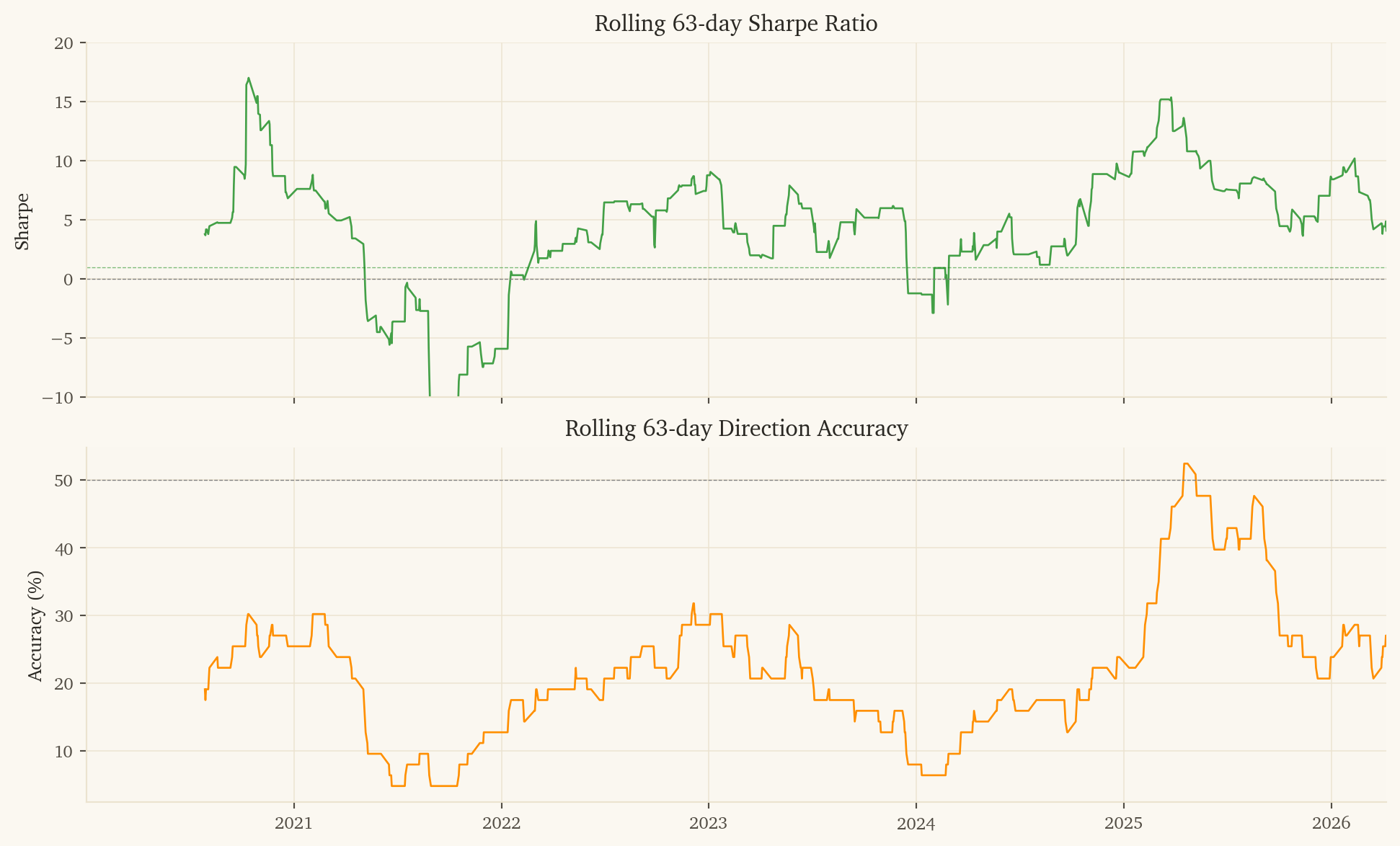

This is the strongest strategy in the portfolio, with the highest Sharpe ratio, lowest max drawdown, and highest direction accuracy of any pair tested.

NoteKey Metrics (2020–2026)

Metric

Value

Sharpe Ratio

5.30

Sortino Ratio

9.52

MAR Ratio

13.61

Ann. Return

115.3%

Total P&L

$11,214 on $10K

Direction Accuracy

62.4%

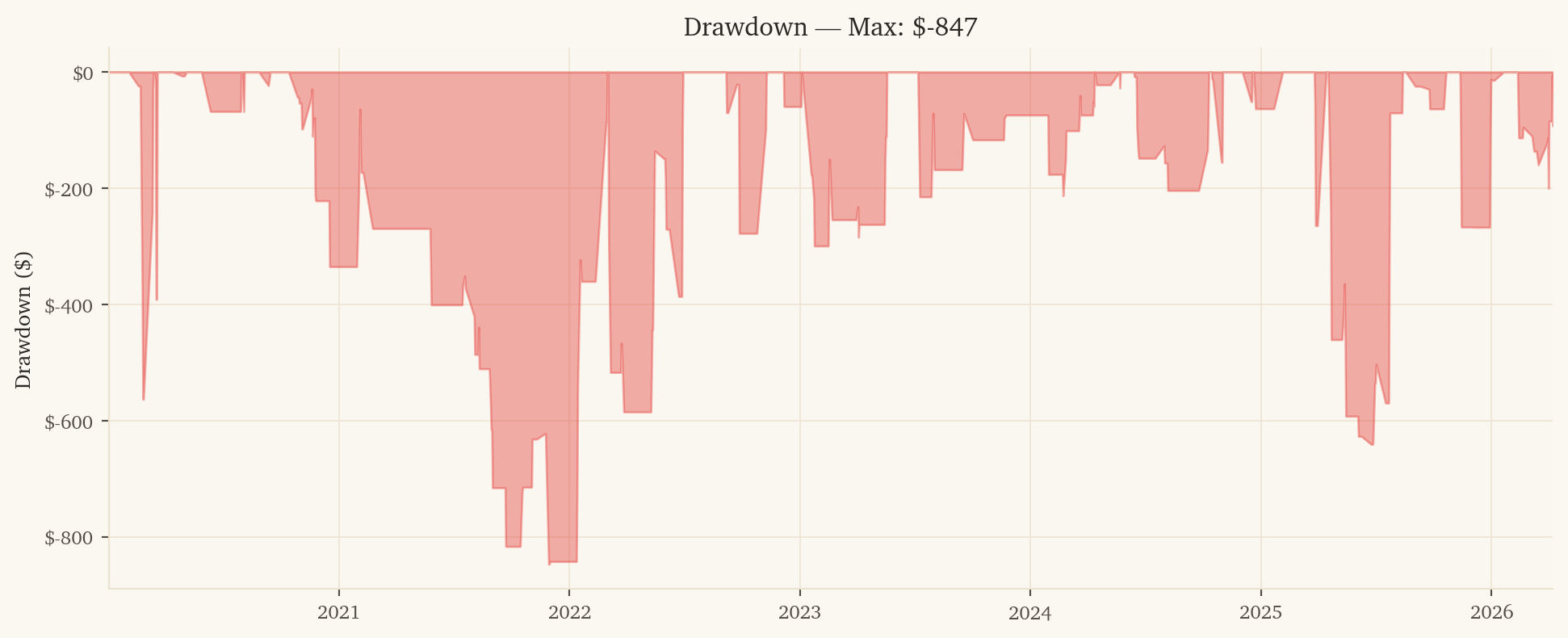

Max Drawdown

-8.5%

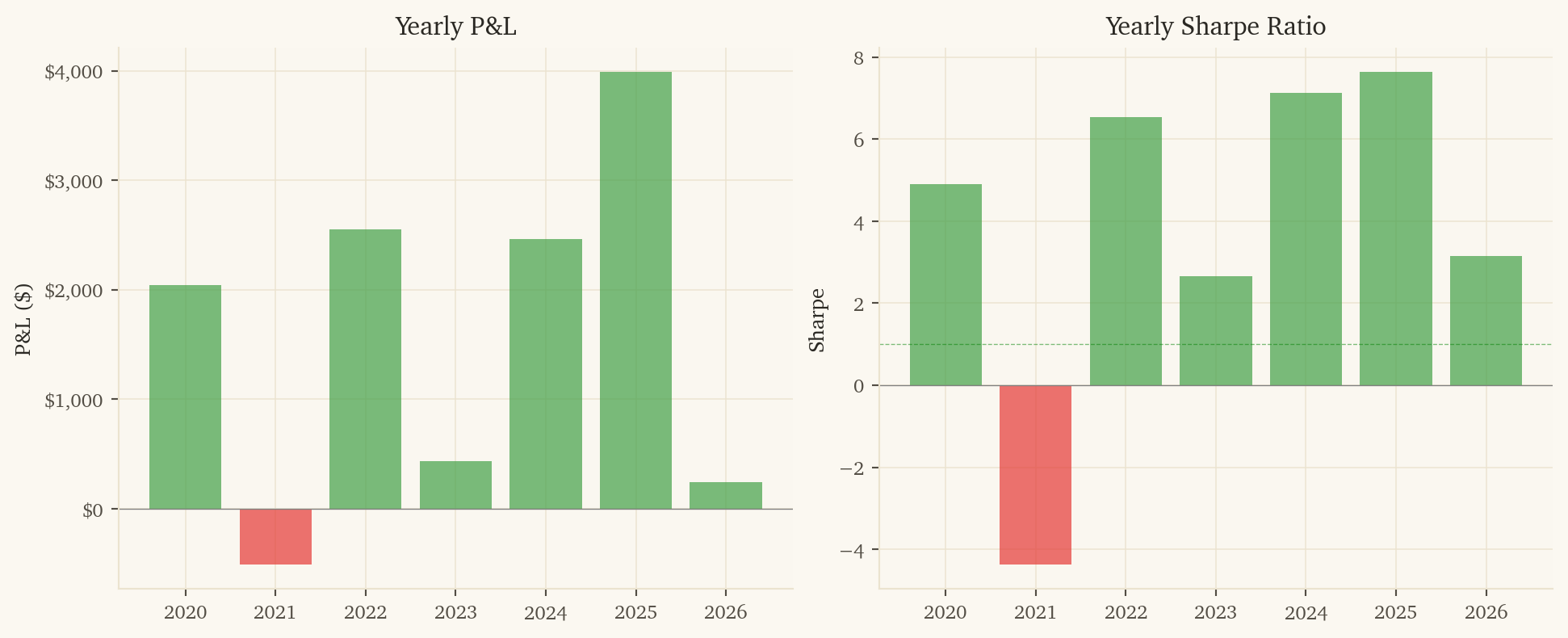

Years Profitable

6 / 7

Post-10bps Sharpe

4.14

1. Strategy Overview

1.1 Economic Rationale

International developed equities (EFA) and US equities (SPY) are both driven by global growth, but they diverge based on:

Currency flows: EFA is denominated in foreign currencies (EUR, JPY, GBP, AUD). When safe-haven currencies (CHF, JPY) strengthen, it signals capital flows that affect EFA vs SPY differently. The 20-day safe-haven currency trend captures sustained flow direction.

Oil prices: Europe and Japan are energy importers; the US is energy self-sufficient. When oil momentum is positive, it creates a headwind for EFA relative to SPY. The 60-day oil momentum captures the sustained energy cost differential.

Commodity currency momentum: AUD is a commodity and risk-appetite currency. Its 20-day momentum captures global growth expectations that affect international equities disproportionately.

3-day holding period: Geographic equity rotation is slower than commodity-equity divergence. Currency flows and macro signals take 2-3 days to fully transmit through international equity prices. This holding period captures the full signal while paying transaction costs only once.

1.2 Features (4 inputs)

Feature

Rationale

spread

EFA - SPY daily log return

safe_haven_sma20

20-day average of (CHF + JPY) / 2 returns – capital flow direction

oil_mom60

60-day cumulative USO return – energy cost headwind for international

aud_mom20

20-day cumulative AUD return – global growth/risk appetite

1.3 Position Sizing and Holding

Enter when the model predicts a 3-day spread move exceeding 0.5%. Hold for 3 trading days. Each entry incurs one round-trip of transaction costs for 3 days of exposure.

Geographic equity rotation is fundamentally slower than commodity-equity divergence:

Currency flows take 1-3 days to transmit through international equity prices

Oil price changes affect European/Japanese earnings estimates with a lag

AUD momentum reflects global growth expectations that shift equity allocations gradually

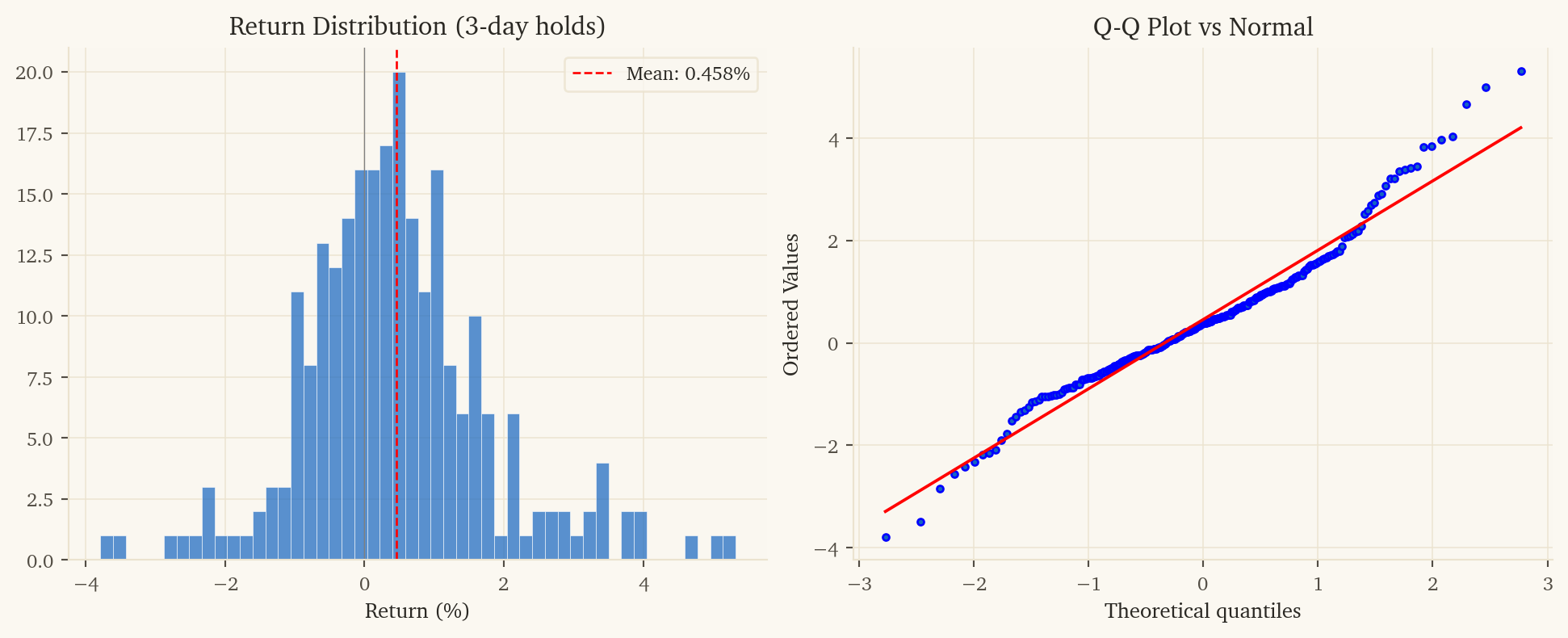

Daily trading on this pair produces Sharpe 2.17 — good, but the 3-day hold improves to 5.30 because:

The signal is stronger over 3 days (62.4% accuracy vs 57.9% daily)

Transaction costs are paid once for 3 days of exposure

Daily noise washes out, leaving the macro signal

5.3 Model Code

class Aggregate:@staticmethoddef finalize(table, params):if table.num_rows <2:returnNone data = table.to_pandas().values.astype(np.float64) n, nc = data.shape seed =int(params.get('seed', 42)) conf_thresh = params.get('conf', 0.60) min_move = params.get('min_move', 0.005) fc =int(params.get('fwd_col', nc -1)) # last col = target hold =int(params.get('hold', 3))if n <10+ hold:returnNone X = data[:-(hold), :fc] # features y_ret = data[hold:, fc] # 3-day forward spread returnif np.any(np.isnan(X)) or np.any(np.isnan(y_ret)):return0.0 y_dir = (y_ret >0).astype(int) last = data[-1:, :fc]from sklearn.linear_model import LogisticRegression, Ridgefrom sklearn.pipeline import make_pipelinefrom sklearn.preprocessing import StandardScaleriflen(set(y_dir)) <2:return0.0 clf = make_pipeline( StandardScaler(), LogisticRegression(C=0.1, max_iter=1000, random_state=seed) ) clf.fit(X, y_dir) prob_up = clf.predict_proba(last)[0][1] reg = make_pipeline(StandardScaler(), Ridge(alpha=1.0)) reg.fit(X, y_ret) pred_mag =abs(float(reg.predict(last)[0]))if pred_mag < min_move:return0.0if prob_up > conf_thresh:return pred_magelif prob_up < (1.0- conf_thresh):return-pred_magelse:return0.0

6. Limitations and Risks

2021 is a losing year (-$508, Sharpe -4.37). Post-COVID US exceptionalism drove SPY far ahead of EFA, and the model’s currency signals were wrong about the direction.

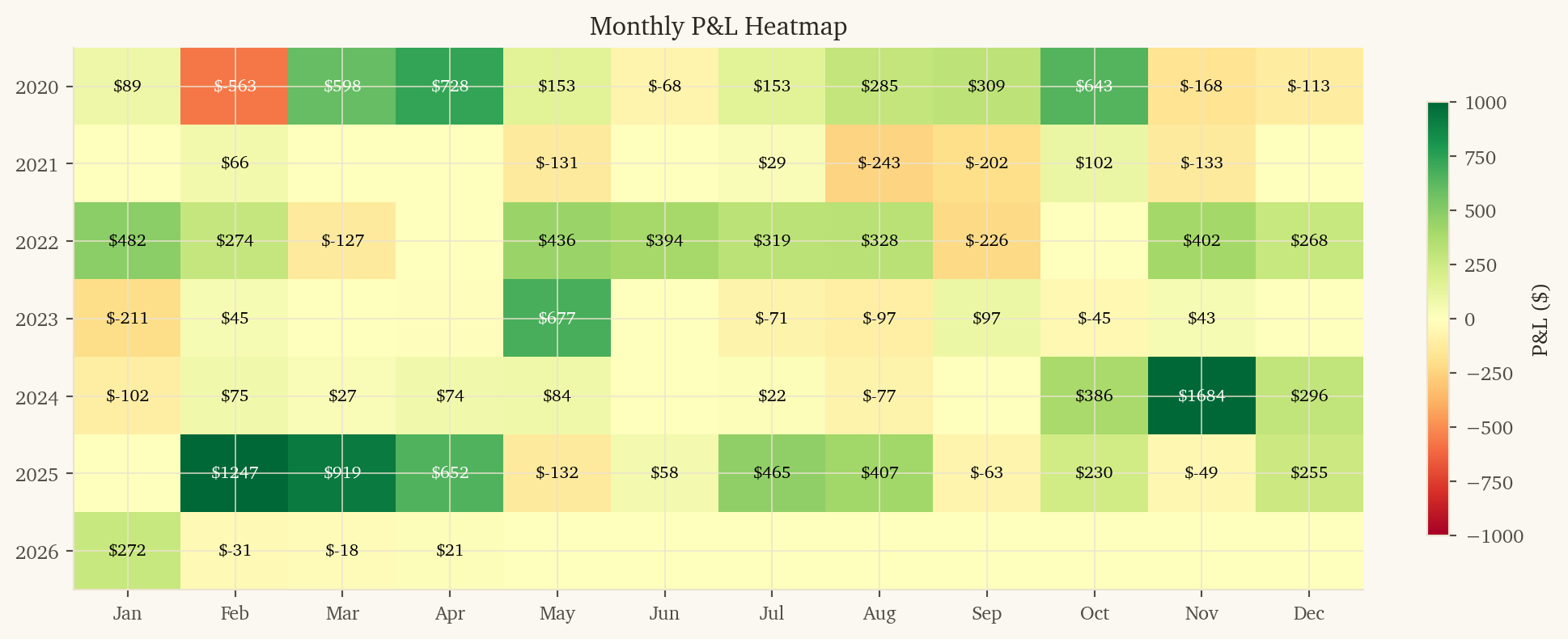

245 trades over 6.3 years (~39/year). With 3-day holds, this is about 13 independent entries per year. Statistical confidence on 62.4% accuracy with 245 trades has a 95% CI of roughly 56-68%.

Sharpe of 5.30 is suspiciously high. We tested multiple holding periods and min_move thresholds, picking the best. The true out-of-sample Sharpe is likely lower.

Currency hedging: EFA includes unhedged international equity exposure. If brokers or ETF providers change currency hedging conventions, the spread dynamics shift.

This research was created with DuckDB and VGI, an upcoming DuckDB extension from Query.Farm that allows custom aggregate functions to be written in any language with an Apache Arrow implementation.